|

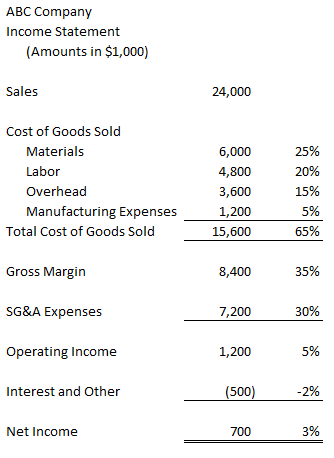

Part One of this series was an introduction to breakeven analysis. It defined what breakeven analysis is and gave a quick example of how it is calculated. This part will talk more about the calculation and using it to analyze a business. Let’s set up an income statement for a sample manufacturing company and then use them to calculate the company’s breakeven amount.  Looking at this we can calculate a breakeven number for the company. The first step is to determine the variable margin, which in sales less the variable costs. The variable costs would be those that vary up and down with sales, the column on the right that is each line’s percent of sales would stay the same for variable costs. In this sample the variable costs would be Materials and Labor. So, the variable margin would be $13,200 [24,000 sales less 6,000 materials and less 4,800 labor]. The variable margin percentage would be 55% [13,200 variable margin divided by 24,000 in sales].

The next step would be to add all the fixed costs up. The total fixed costs are $12,500 [3,600 Overhead + 1,200 Mfg Expenses + 7,200 SG&A Expenses + 500 Interest and Other]. From our calculations above we know that each dollar in sales results in 55 cents of variable margin. We now have all the elements for the breakeven calculation. Breakeven is equal to Fixed Costs divided by the Variable Margin. So, our breakeven would be $22,727 [12,500 divided by 0.55]. And what do we do with this number? Read on. Now that you know the breakeven numbers you can use this as a diagnostic tool for quickly analyzing financial statements. For our example, say the next period’s income statement shows sales of $20,000 and a loss of $1,500. You can easily see that because sales were less than the breakeven number, we didn’t have enough sales to cover our fixed costs. What if sales were over breakeven, but we still had a loss. You can check the components of your breakeven calculation for the period to see what’s off. Is the variable margin lower? Are the fixed costs higher? Looking at it this way, you’ll be able to easily know what to focus on so you can explain the financial results. My next post in this series will focus on using breakeven analysis in a more focused way.

2 Comments

Hello all. I’m sorry I’ve been away from the site for a while with Christmas busyness and other things. I’m back and writing again. I started a series with my last post, and I will get back to that. But for my first post of 2020 I wanted to talk about New Year’s resolutions.

Businesses make New Year’s resolutions. But they call them “budgets” and “strategic plans”. They help them to know where they are going and how well they do things. They expect to measure themselves against these goals. We make “New Year’s resolutions” and nobody really expects to keep them. I’d like to recommend to you that you take your resolutions and turn them into goals. Have a strategic plan for yourself; both career-wise and for your life. Make them something that you will track and will also achieve. You may not reach all your goals. Businesses often miss their budgets. But in the trying and in the measuring yourself against them, you will have a better understanding of yourself. One of my goals for this year is going to be to write blog posts regularly every other week. So far, I’m on track for the year. (For the decade also!) Check back in two weeks to see if I can keep it up. Have a great year. |

RSS Feed

RSS Feed